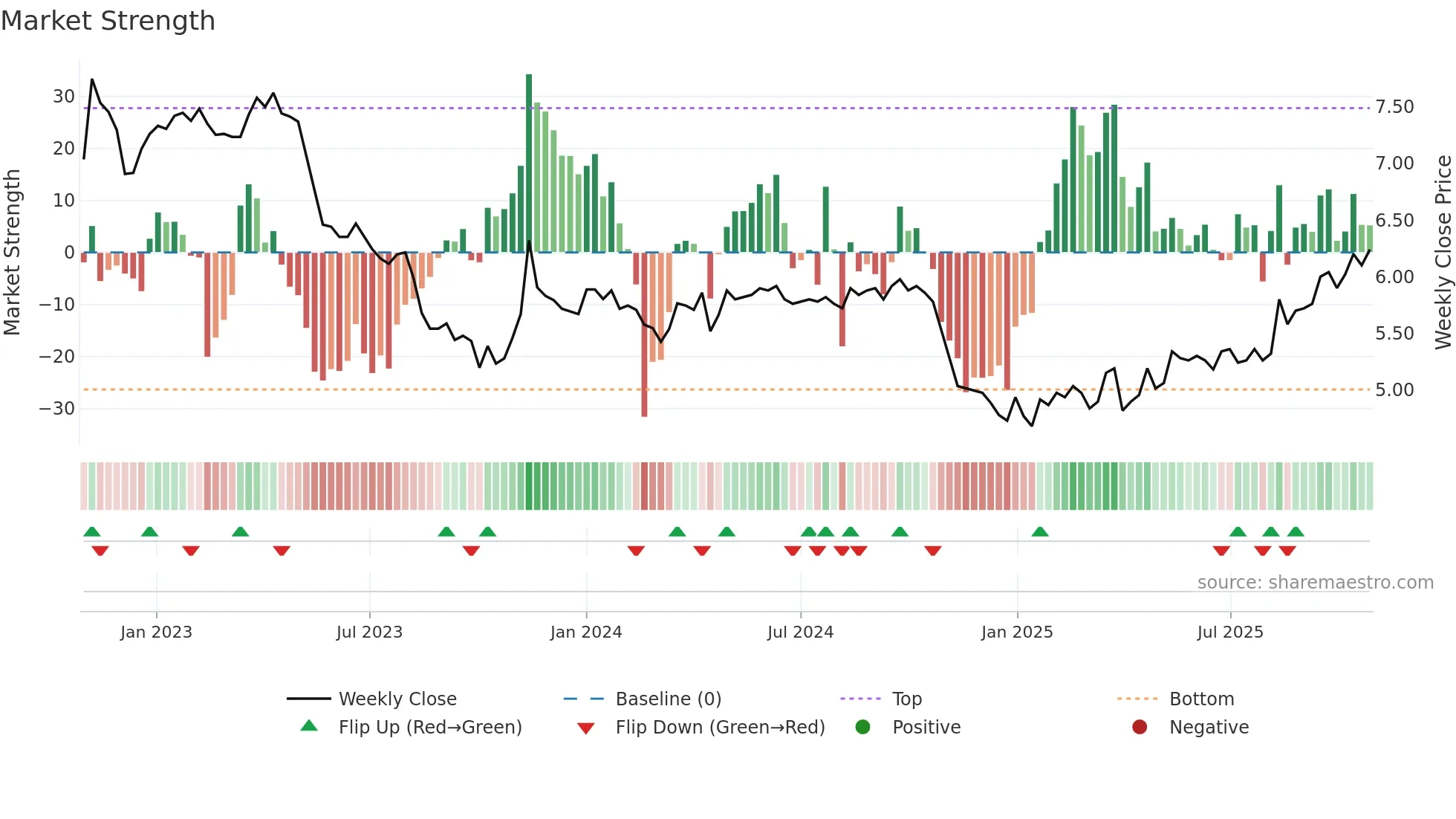

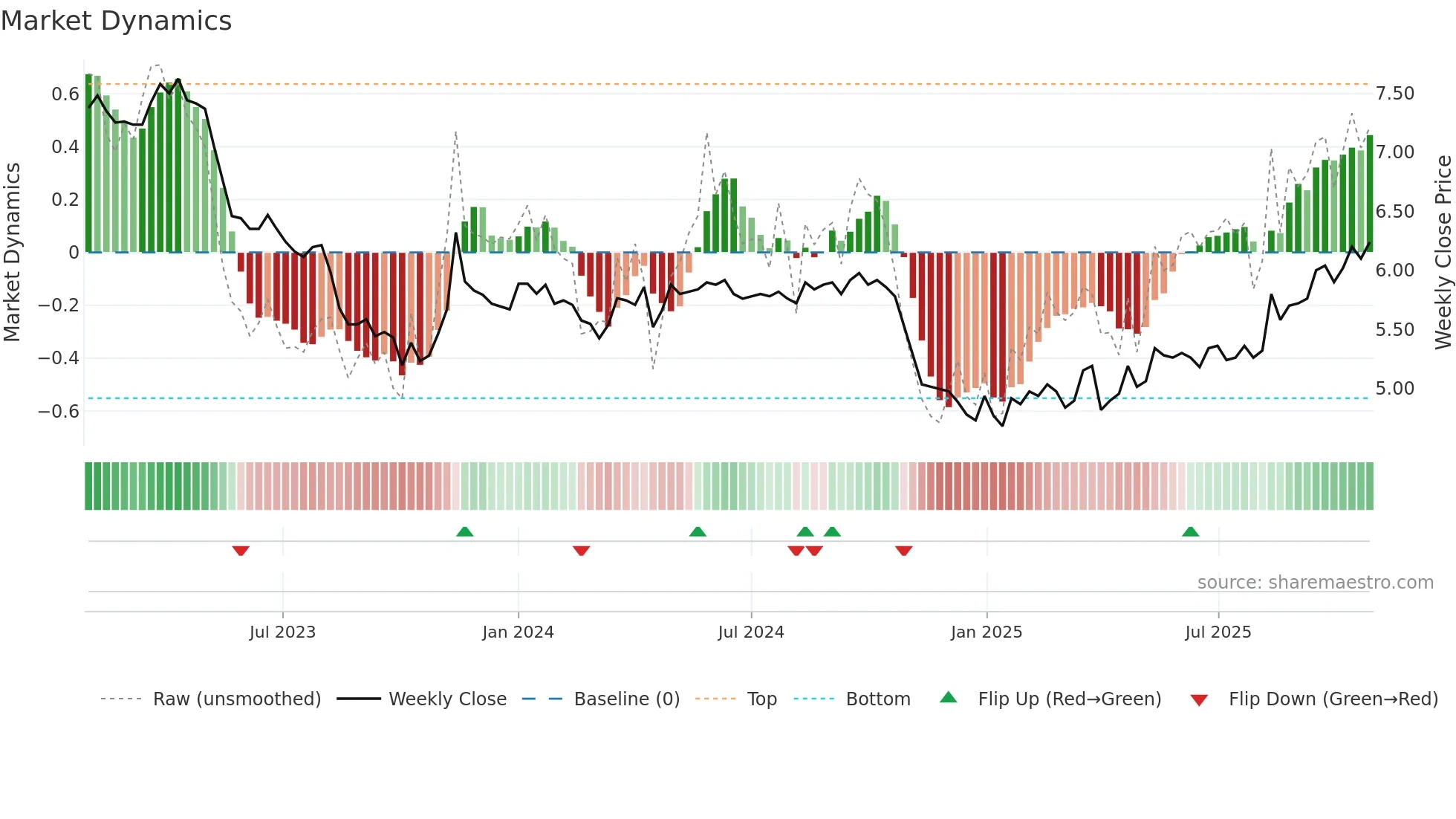

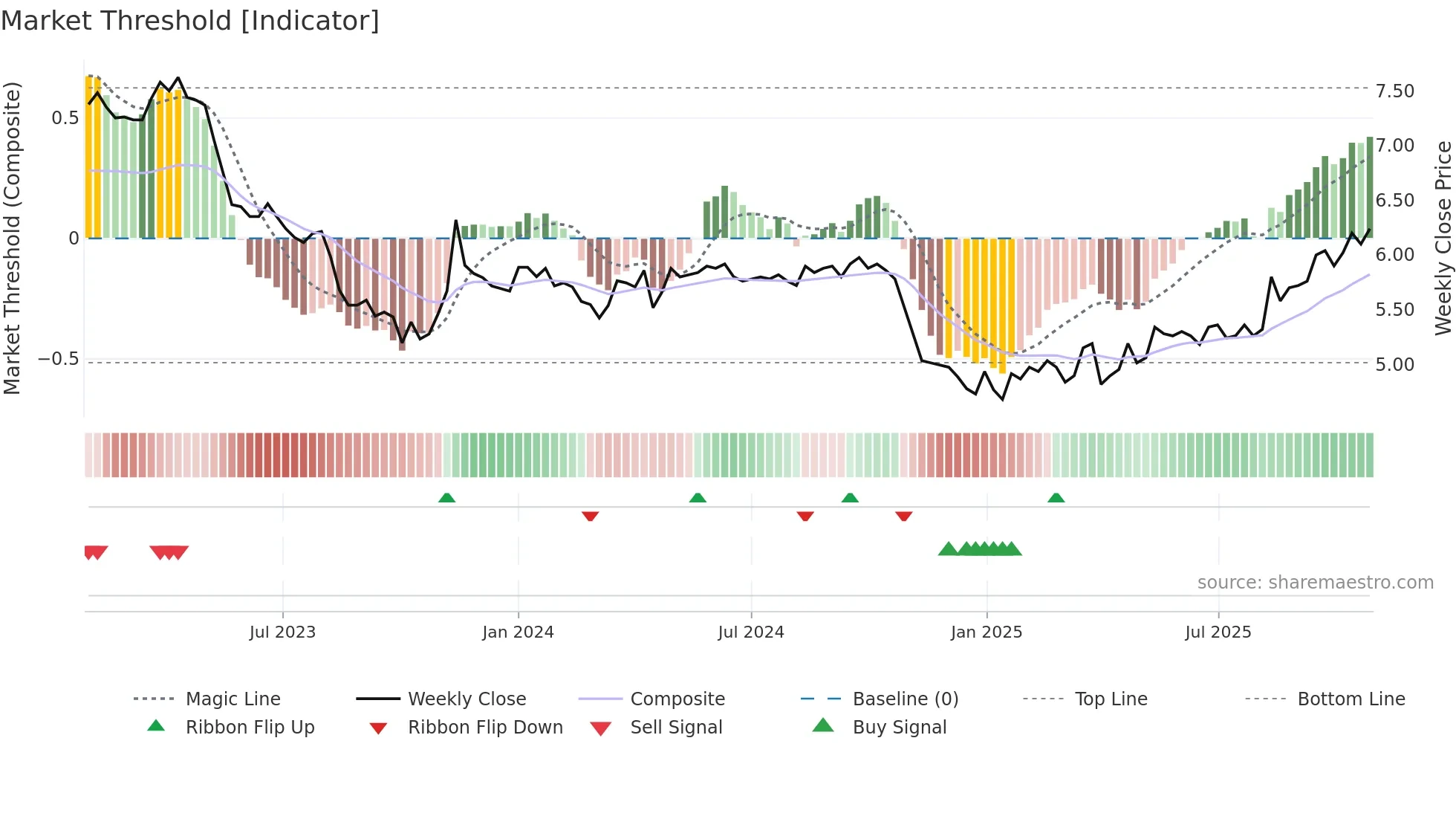

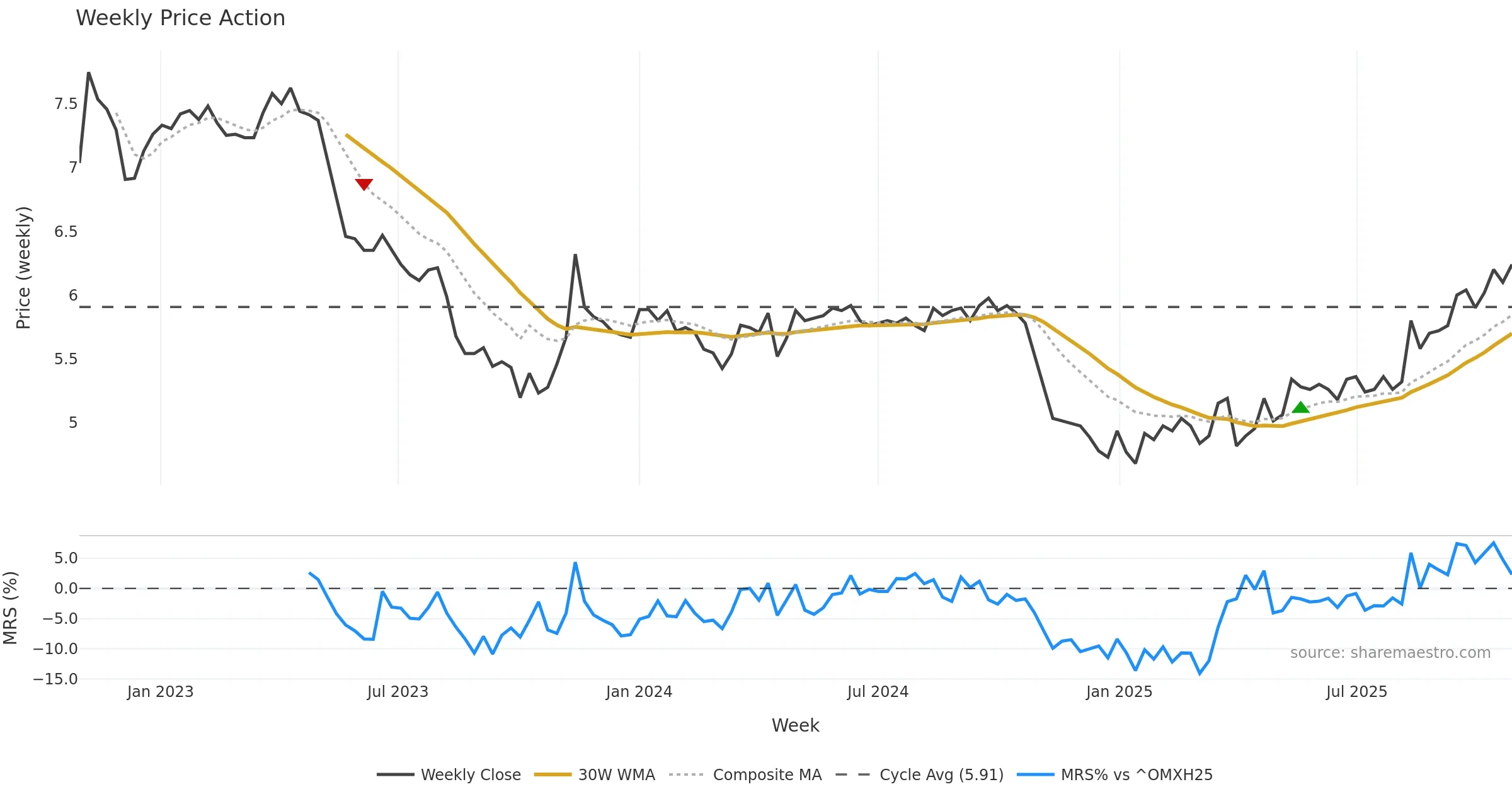

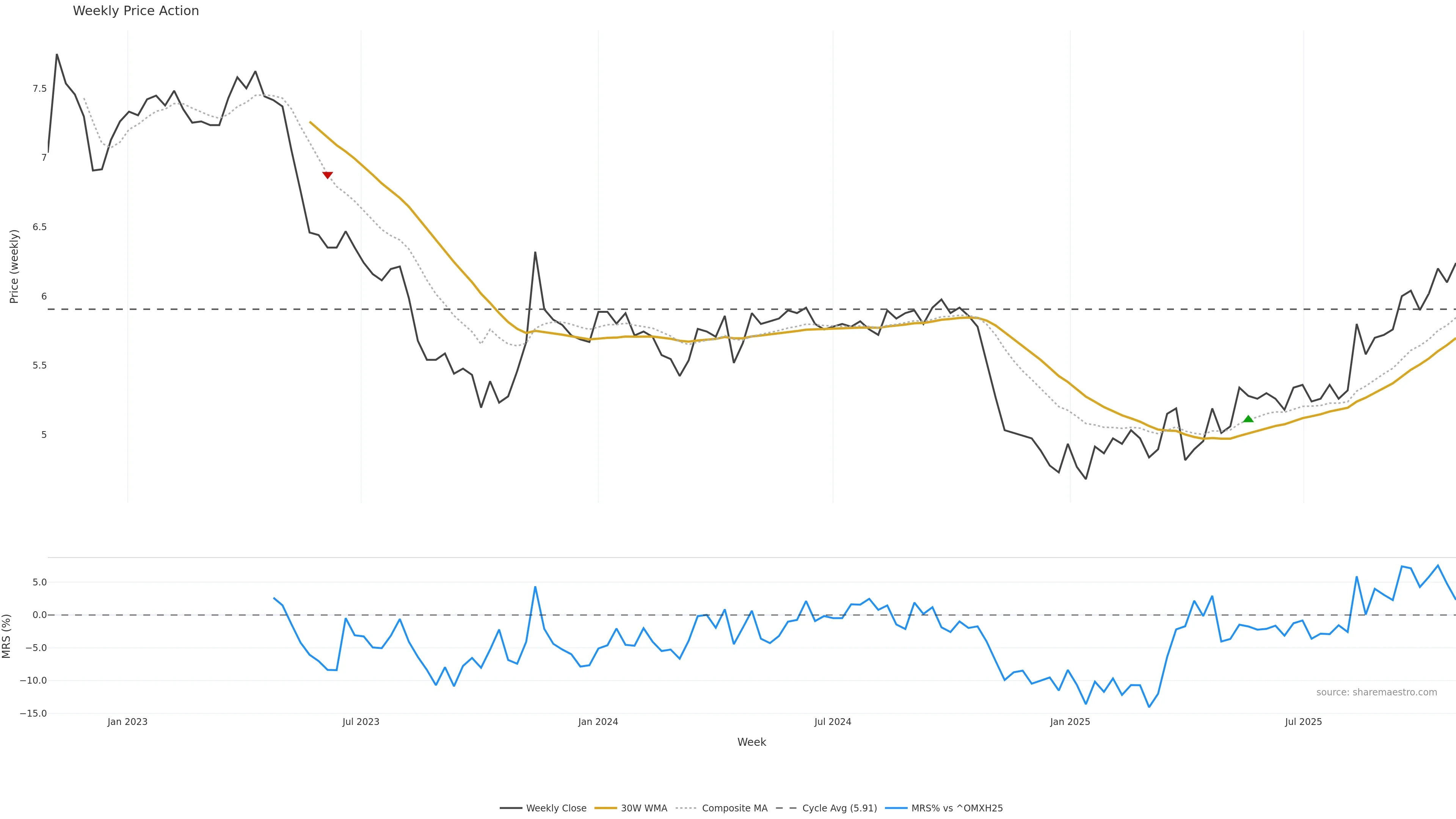

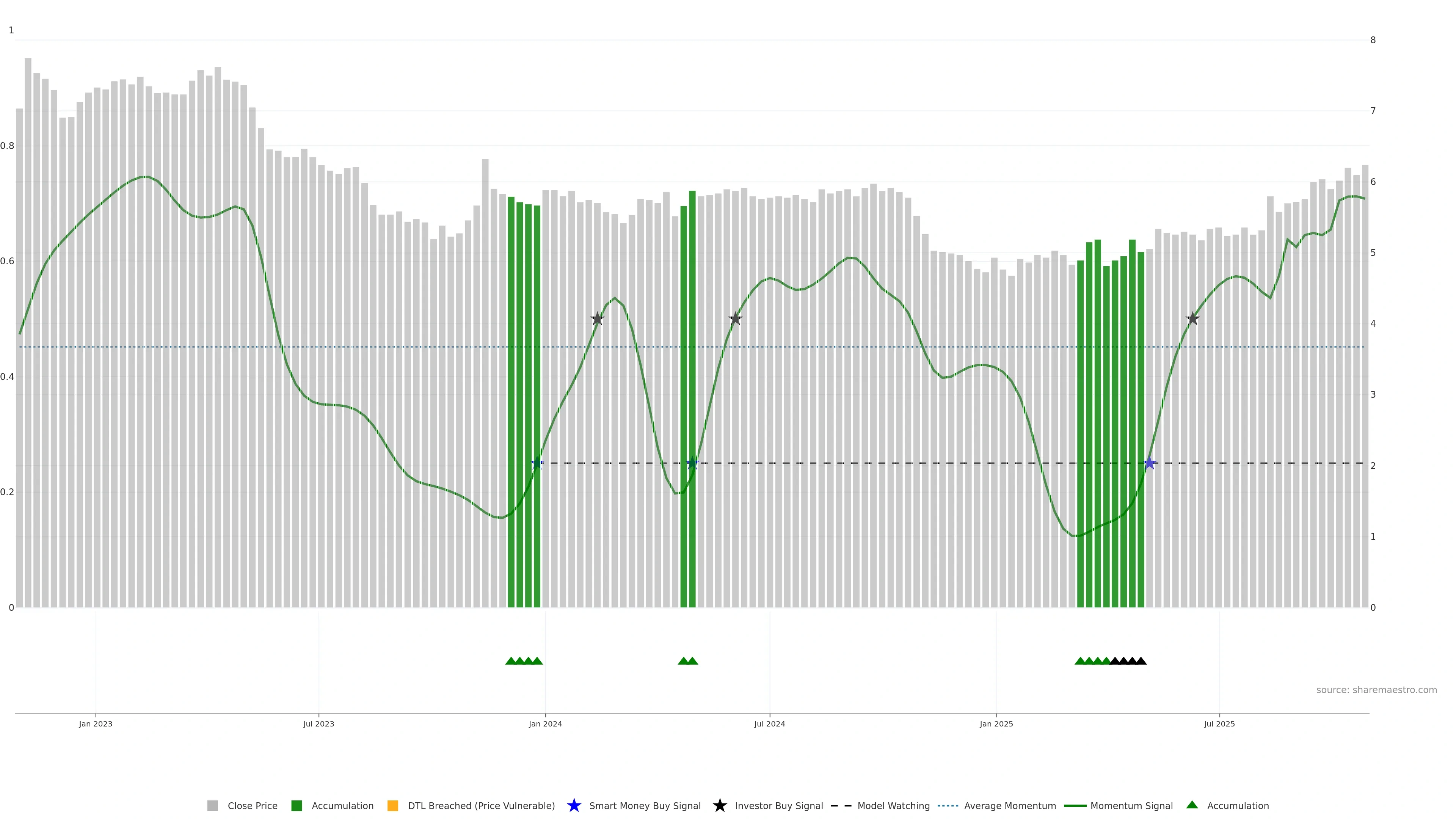

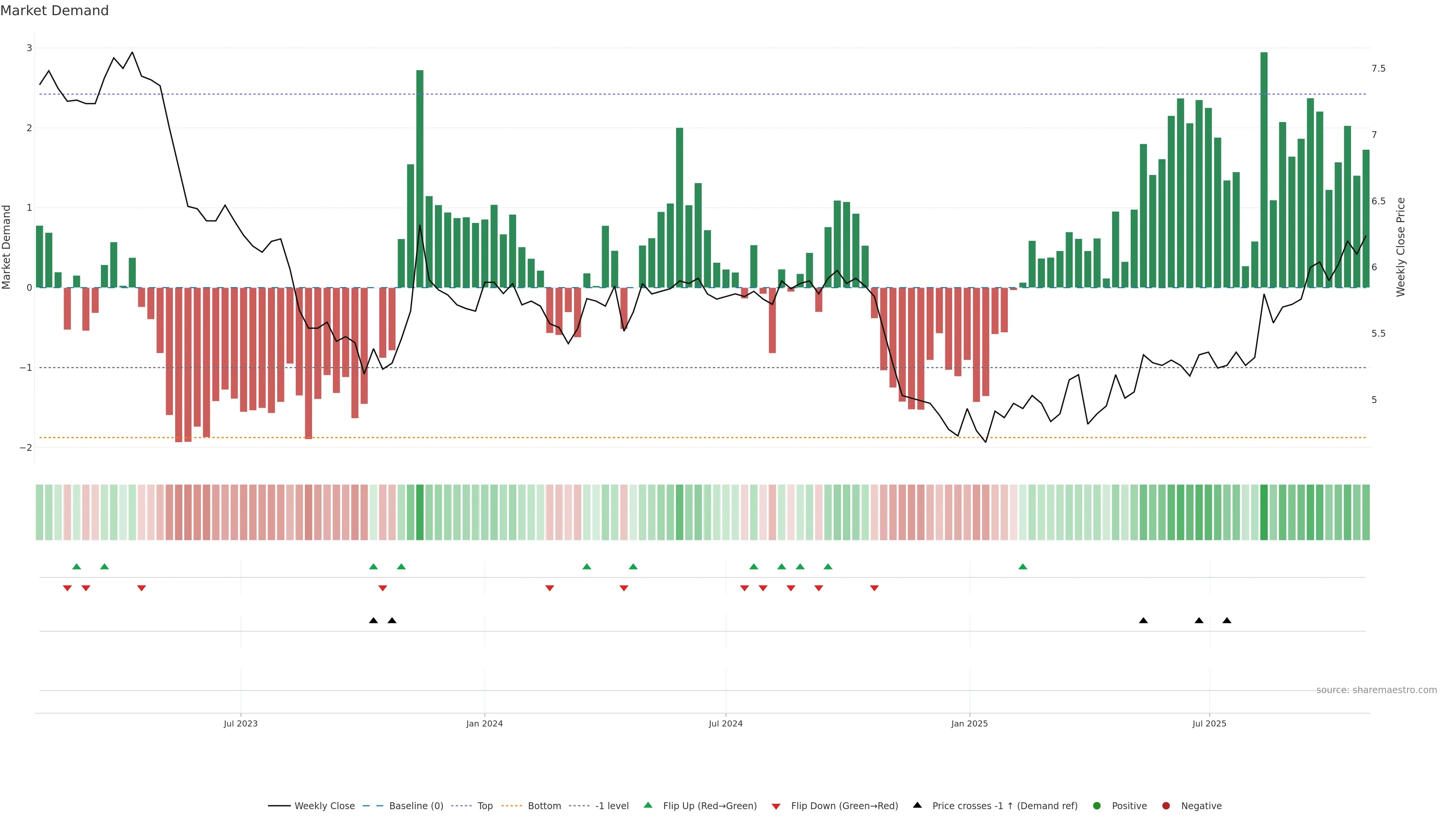

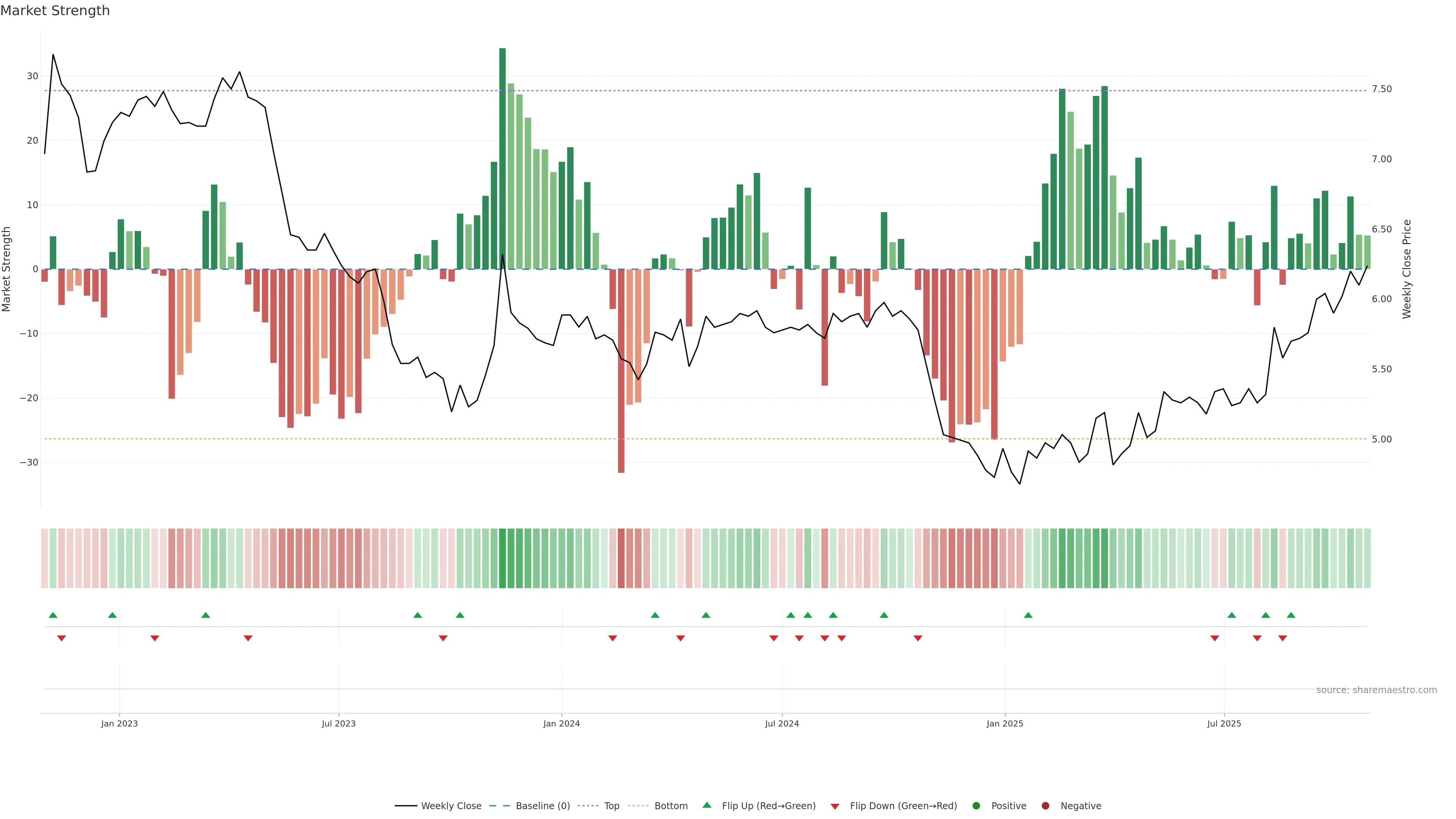

Market Regime (Activity)

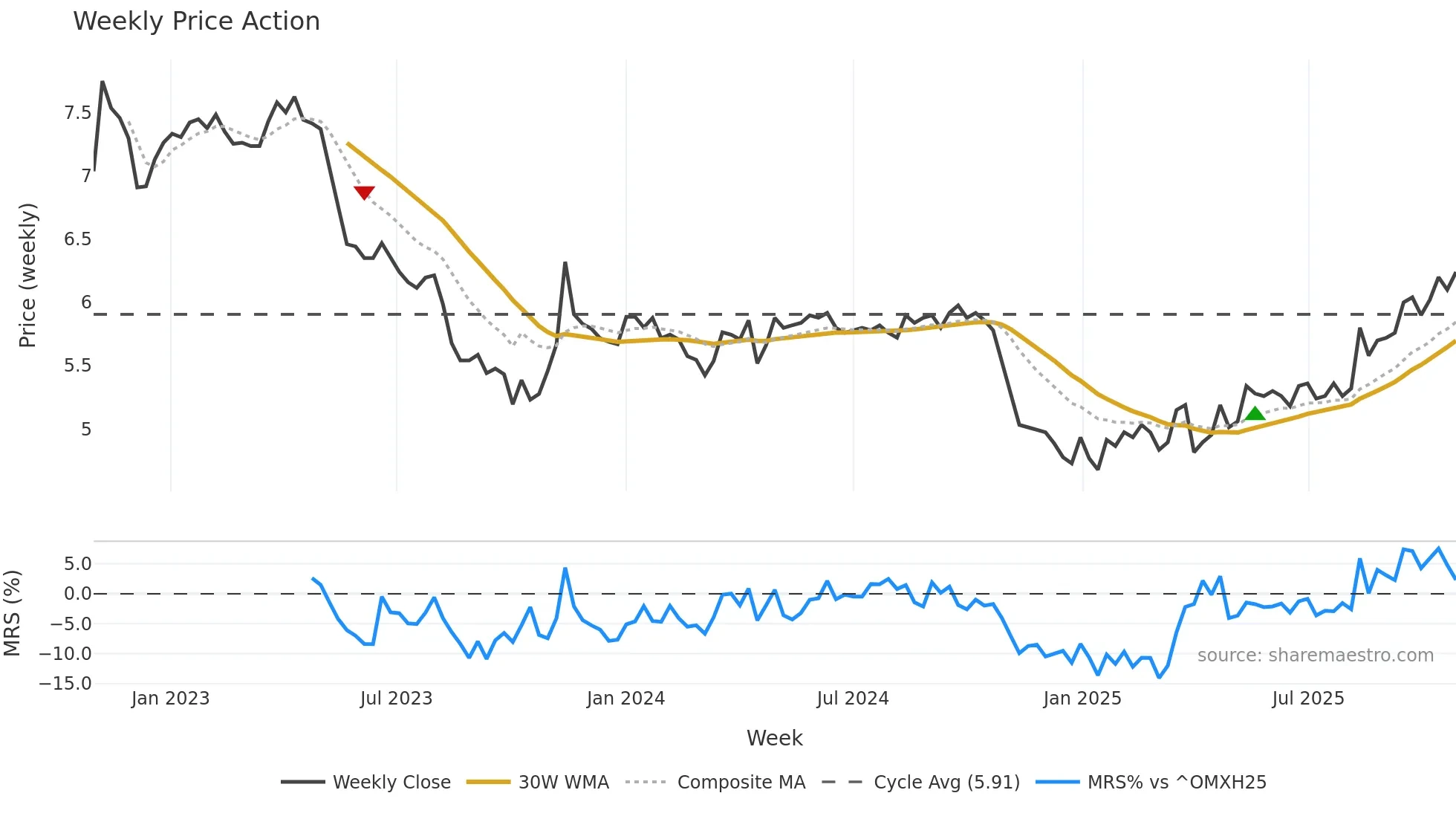

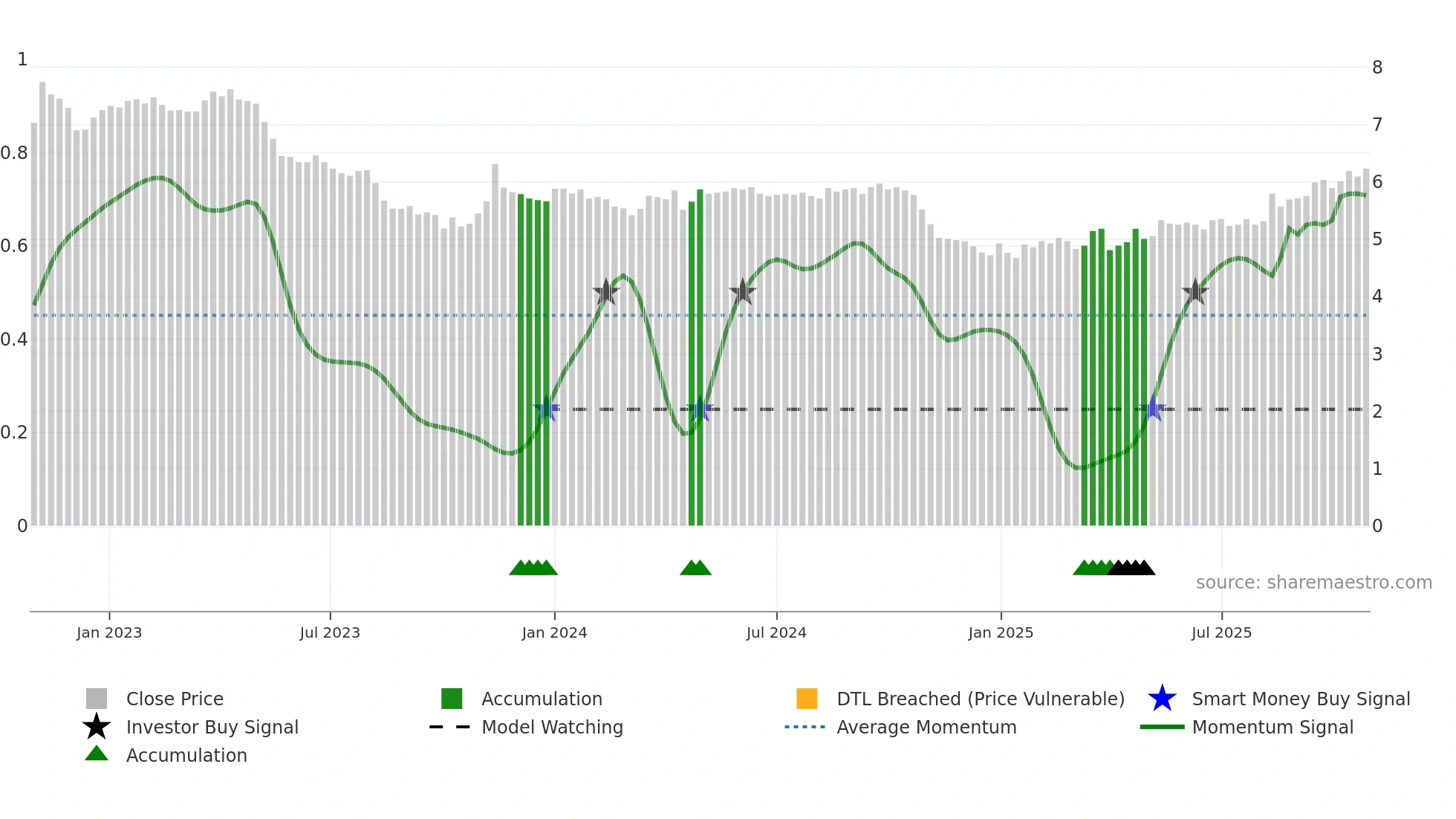

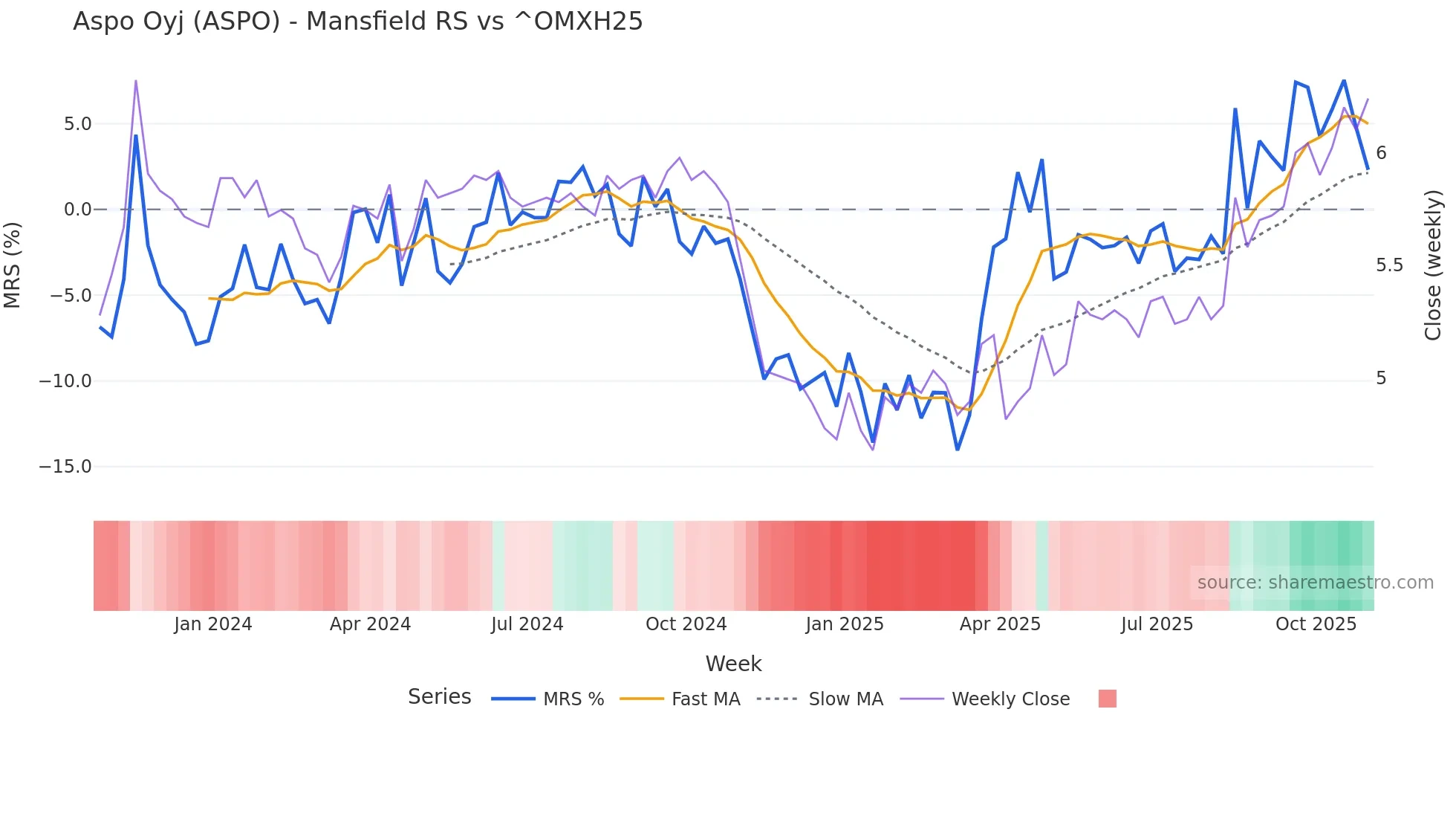

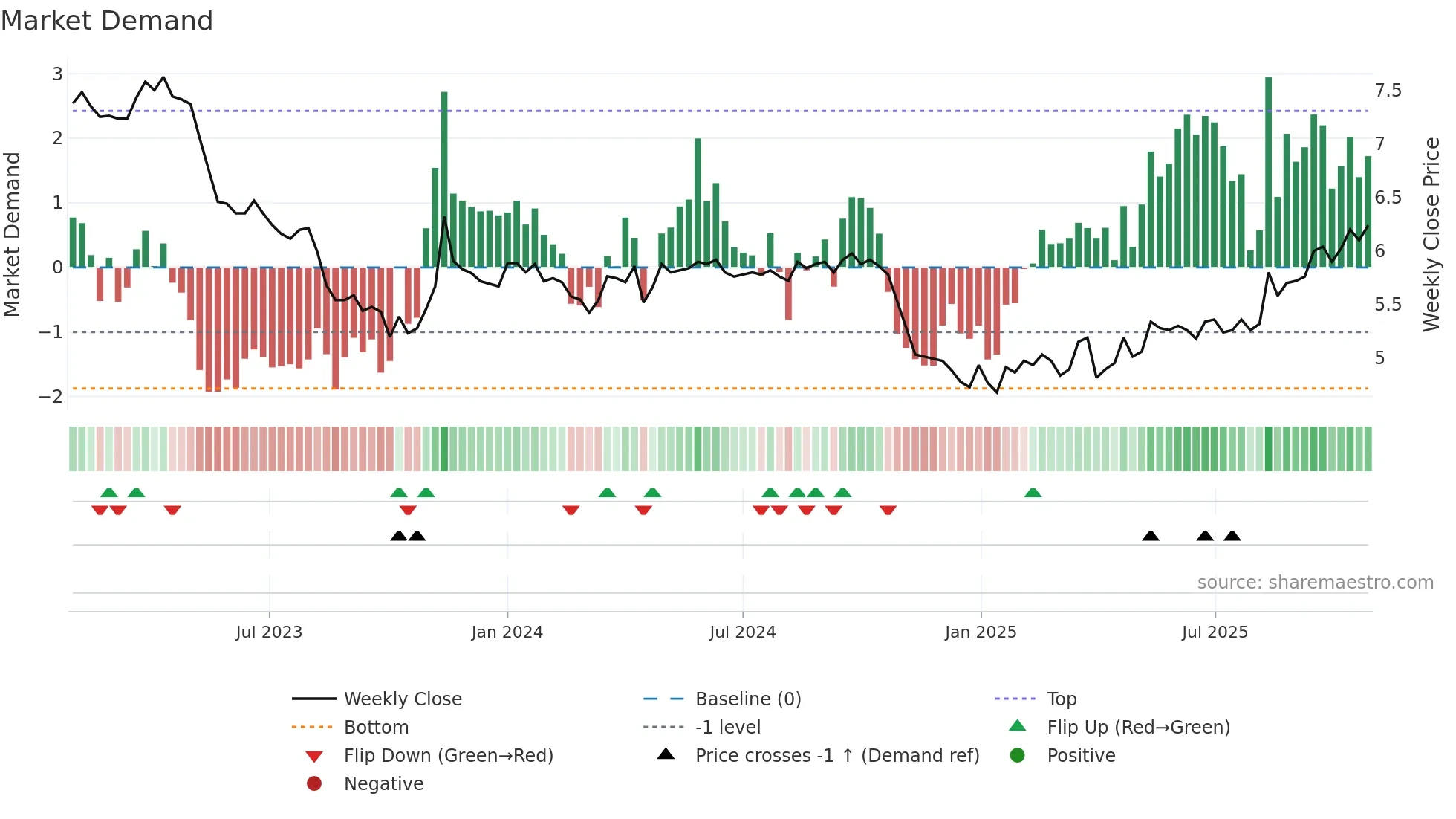

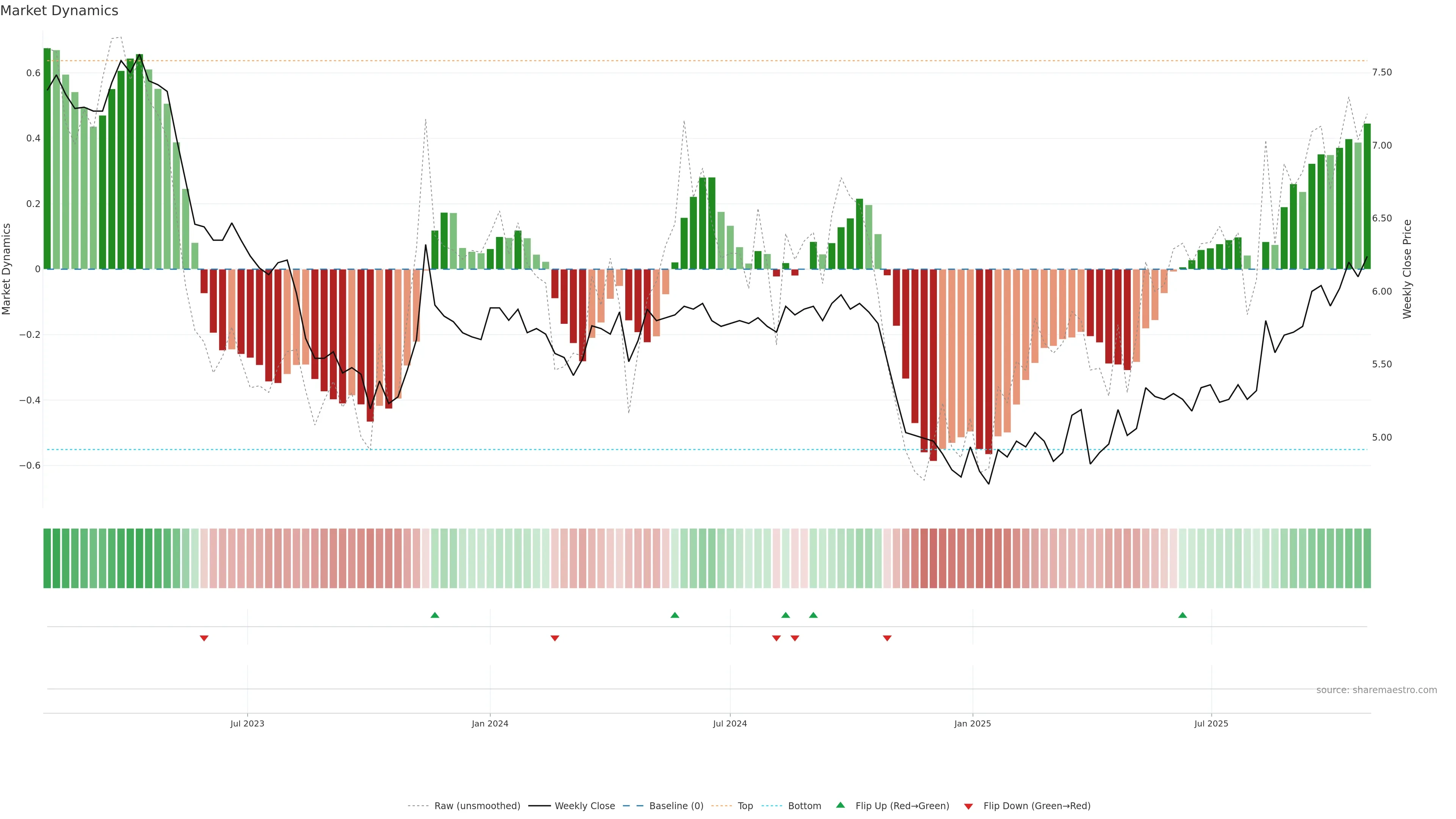

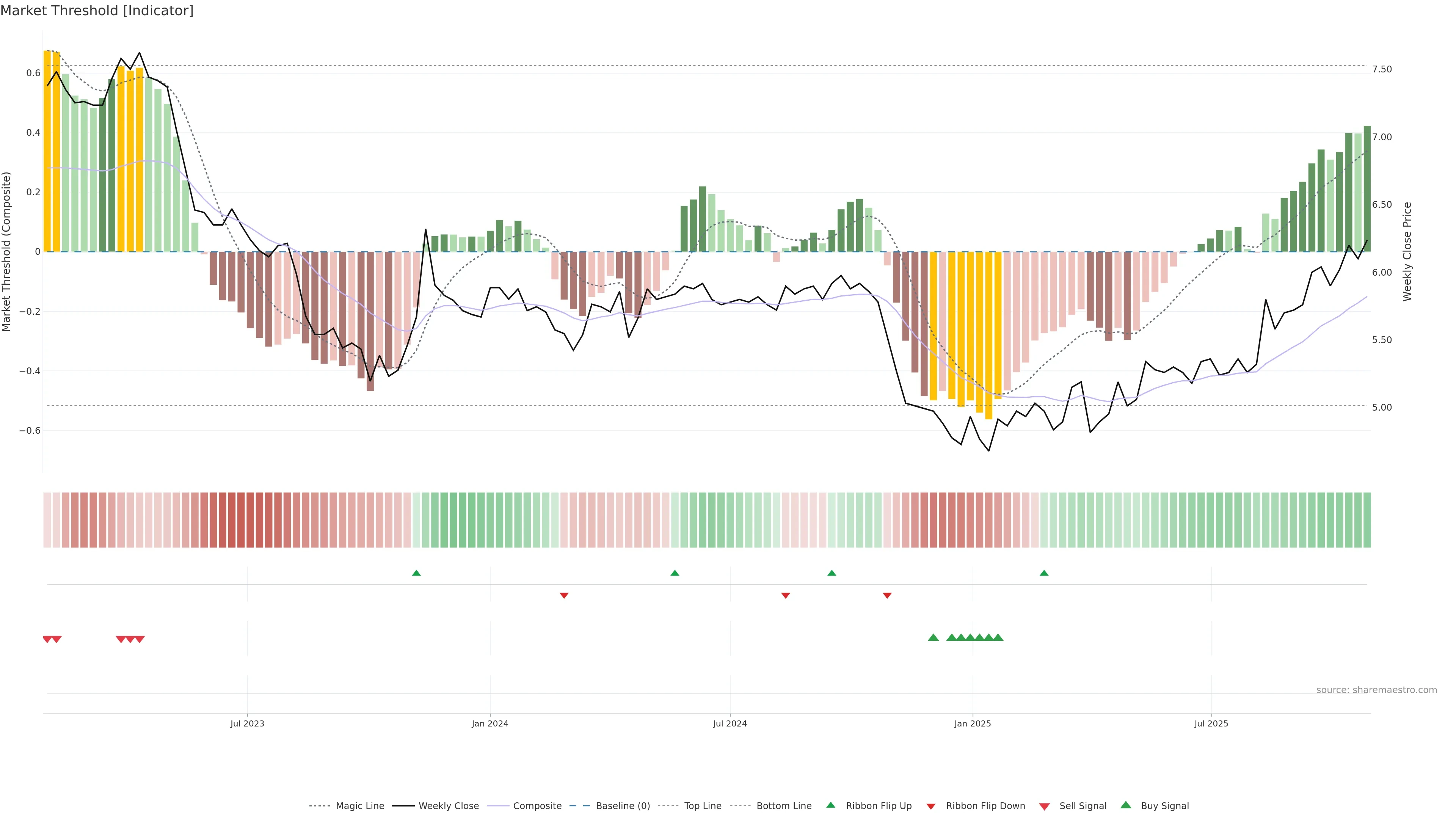

Market activity regime is constructive and improving. — Constructive regimes increase odds of follow-through.

Score 0.5

+1 / -0

Level 0.032

Market activity regime is constructive and improving.

Market activity regime is constructive and improving. Constructive regimes increase odds of follow-through. In essence this reflects activity/volatility regime (constructive vs corrective) with a bullish tilt.

pol 0.5

conf 0.6

moderate · medium

What it means

Market activity regime is constructive and improving. Constructive regimes increase odds of follow-through. In essence this reflects activity/volatility regime (constructive vs corrective) with a bullish tilt.

Implications

Improves odds for follow-through if pullbacks hold higher lows. (pol 0.50, conf 0.60 → moderate/medium)

No additional observations.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}