In brief

Nassim Nicholas Taleb is best known for The Black Swan, but his influence reaches beyond a phrase that entered market language. His work links options trading, fat-tailed probability, barbell risk taking, antifragility, and a fierce critique of institutions that harvest gains while exporting losses. This profile examines his trading roots, intellectual system, influence on tail-risk investing, criticisms, and continuing relevance.

- Taleb's market importance comes from turning options-trading experience into a public theory of uncertainty, rare events, and fragile systems.

- His barbell idea favors a combination of extreme safety and controlled exposure to high-upside uncertainty rather than middle-risk portfolios that depend heavily on models.

- Universa Investments, where Taleb has served as a scientific adviser, became the most visible institutional expression of his tail-risk logic, with reported crisis-period payoffs in 2008 and 2020.

- The main limitation of Taleb's approach is not the insight that tail risk matters, but the difficulty of funding, sizing, governing, and communicating convex protection through long periods when it looks wasteful.

- His critics argue that he overstates the uselessness of statistical practice, underplays existing work on fat tails and robust methods, and sometimes weakens his case through polemical style.

Performance and evidence

Performance markers

Visual Evidence

Charts and timelines

Risk

Timeline

Philosophy

Performance

The trader who made catastrophe the starting point

Nassim Nicholas Taleb built his public reputation by asking Wall Street to look where it least wanted to look. Not at the smooth middle of the distribution, where models are comfortable and committees can speak in decimals, but at the tails, where a trade, a firm, or an entire financial system can be ruined. His subject was not panic as a mood. It was panic as a structural fact, the point at which the mathematics of ordinary days stops behaving like ordinary mathematics.

That insistence made him a strange figure in finance. Taleb was not simply a trader who wrote, or an academic who criticized traders from a safe distance. He came out of derivatives, where the value of a position can change violently when markets gap, volatility jumps, liquidity disappears, or assumptions break. He then turned that experience into a broader attack on false precision, success stories, risk models, and institutions that mistake calm for safety.

His importance lies in the conversion of an options trader's instinct into a durable theory of market survival. Fooled by Randomness gave investors a language for luck masquerading as skill. The Black Swan gave them a metaphor for rare, high-impact events and the failures of hindsight. Antifragile pushed the argument further, asking which systems can gain from disorder. Together, they made Taleb one of finance's most influential skeptics of certainty.

Why Taleb matters in modern finance

Taleb matters because the central risk in finance is not volatility alone. It is ruin. A portfolio can survive daily fluctuation and still be structurally fragile if it is exposed to a discontinuous loss. A bank can look conservative under standard measures and still be vulnerable to funding runs, crowded trades, correlated balance sheets, or policy shocks. Taleb's core contribution was to shift attention from average outcomes to survival across states of the world that models tend to treat as remote.

That shift changed how many investors talk about risk. After the financial crisis of 2008, the phrase Black Swan moved from a book title into market shorthand. It was often overused, sometimes badly, but its spread reflected a real institutional discomfort: models built on recent data had failed to capture how leverage, liquidity, incentives, and panic interact. Taleb's work did not explain every detail of the crisis, but it captured the embarrassment of risk systems that appeared sophisticated before they proved brittle.

His influence also comes from the moral edge of his argument. Taleb's objection is not merely that people mismeasure risk. It is that many people profit from mismeasured risk, especially when they keep the upside and shift the downside to clients, taxpayers, employees, or future stakeholders. In that sense, his finance writing is inseparable from his ethics. For him, a hidden tail exposure is not just a bad trade. It is often a transfer of fragility from the visible winner to someone else.

From derivatives desks to a theory of uncertainty

The foundation of Taleb's authority is practical, not purely literary. NYU Tandon describes him as a former derivatives trader who spent more than two decades specializing in options and probability problems before becoming a scholar of risk engineering. Wiley's description of his 1997 book Dynamic Hedging places him squarely inside the world of professional derivatives practice, emphasizing exotic options, hedging, arbitrage, liquidity, correlation, and the practical monitoring of portfolio risk.

Dynamic Hedging is important because it shows the early Taleb before the aphorisms, feuds, and broad social theory. The book is technical and practitioner-oriented. It treats options not as textbook abstractions but as living instruments with path dependence, liquidity holes, and hidden exposures. The table of contents itself reads like a map of the concerns that would later become public themes: beware the distribution, understand gamma, respect volatility, and do not assume that pricing formulas eliminate trading risk.

This origin matters because Taleb's later critique of financial models was not a rejection of mathematics by a literary outsider. It was a critique from someone who had lived inside model-driven markets. He did not argue that quantitative tools are useless in all settings. His sharper claim was that tools become dangerous when users confuse tractable assumptions with the structure of reality, especially when small probability estimates determine large exposures.

Empirica and the inversion of Wall Street psychology

The clearest early portrait of Taleb's trading philosophy came in Malcolm Gladwell's 2002 New Yorker profile, which described Empirica Capital as a firm built around a psychological inversion. Many market participants sold options, collected steady premiums, and looked skilled until a large move arrived. Empirica sought the other side: positions that often lost small amounts but could pay off dramatically when the market moved far enough or fast enough.

That structure was emotionally difficult by design. It meant accepting frequent small disappointments, looking wrong for extended periods, and resisting the human preference for steady confirmation. In a financial culture that rewards smooth return streams, this was almost antisocial. The trader selling catastrophe insurance can look prudent for years, while the buyer can look wasteful. Taleb's point was that appearances can reverse in a day when the hidden distribution finally reveals itself.

Empirica was less a conventional hedge fund story than a laboratory for a worldview. It embodied the idea that the right question is not whether a strategy wins often, but what happens when it loses and what happens when it wins. A position that wins most months but risks extinction is not superior to one that bleeds modestly while preserving the possibility of a large convex gain. This became one of Taleb's most persistent attacks on market performance culture.

Fooled by Randomness and the assault on market hero stories

Fooled by Randomness appeared as a market book, but its real target was the way humans convert lucky paths into biographies of skill. Penguin Random House presents the book as part of the Incerto, Taleb's broader investigation of opacity, luck, uncertainty, probability, human error, risk, and decision-making in a world that resists full understanding. That frame is essential. The book is not just about traders. It is about the tendency to mistake a favorable sample path for proof of competence.

In markets, the mistake is especially costly because the number of participants is large and the feedback is noisy. If enough traders take enough risks, some will prosper for reasons that are indistinguishable from skill in the short run. Capital then flows toward the survivors. Their methods are imitated. Their confidence rises. The losers disappear from the story. Taleb made that survivorship problem vivid by emphasizing that observed success is only one version of what could have happened.

The argument cut against one of finance's favorite habits: explaining performance after the fact. Taleb did not deny that skill exists. He denied that financial success reliably reveals it. That distinction remains uncomfortable for allocators, consultants, managers, and journalists because the industry depends on narrative. A manager with a five-year record needs a process story. Taleb's warning is that the story may be true, false, or simply under-tested against the paths that did not occur.

The Black Swan as a market idea, not just a phrase

The Black Swan turned Taleb from a respected market skeptic into a public intellectual. The book's title became a shorthand for rare, high-impact events that are explained afterward as if they had been obvious. Yet its market meaning is narrower and more useful than the way the phrase is often used. A Black Swan is not merely a bad surprise. It is an event whose impact is large, whose probability was poorly represented beforehand, and whose explanation is often cleaned up in hindsight.

That distinction matters because finance is full of events that are not truly unimaginable. Crashes, defaults, pandemics, liquidity freezes, and policy shocks have precedents. What often fails is not imagination but preparation. Taleb's practical emphasis is less on naming the next disaster than on building portfolios and institutions that are not destroyed by the failure to name it. The book's popularity was partly due to timing, but its durability came from this deeper point about ignorance and exposure.

The book also intensified Taleb's critique of Gaussian comfort. In markets with fat tails, the extreme observation is not a rounding error at the edge of the model. It can dominate long-run outcomes. That is why his writing repeatedly returns to asymmetry. If losses are capped and upside is open, uncertainty can be a friend. If gains are small and steady while losses are open-ended, uncertainty is a predator disguised as income.

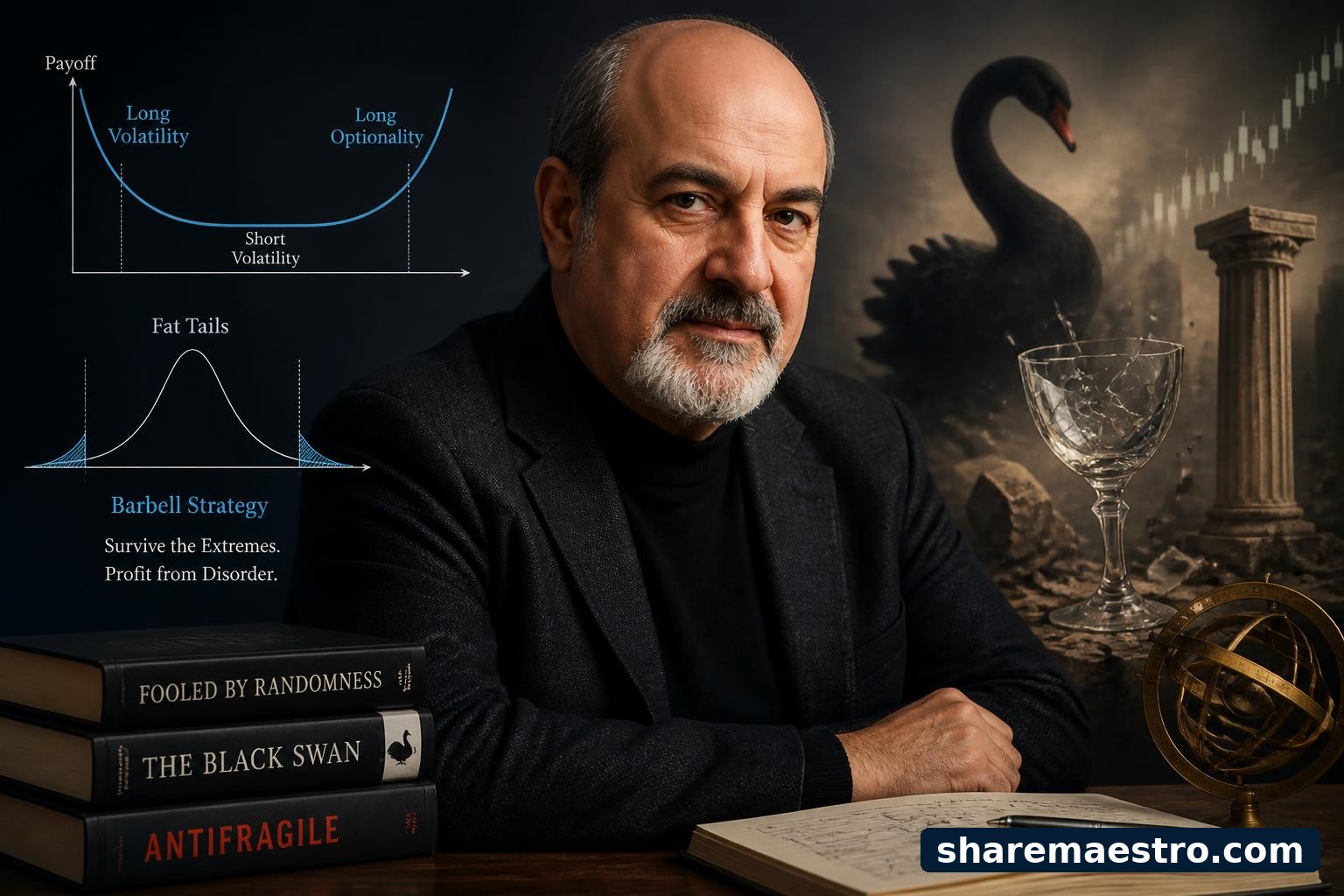

The barbell as architecture, not slogan

Taleb's barbell is often summarized too casually. It is not a magic allocation, nor a universal formula. Its logic is to avoid exposures that look moderate but depend heavily on model accuracy. On one side of the barbell sits safety, liquidity, and survival. On the other side sits a smaller set of speculative or convex exposures where the downside is limited and the upside can be large. The middle is suspect when it offers neither true safety nor true optionality.

In an EconTalk discussion of antifragility, Taleb described a portfolio with a large allocation to Treasury bills and a smaller allocation to very risky securities as more robust than a seemingly balanced portfolio, provided the safe side is genuinely safe for the purpose at hand. The reason is not that the risky sleeve is safe. It is that its risk is known and bounded by size, while the supposedly moderate portfolio may contain hidden dependence on correlations, volatility estimates, and liquidity assumptions.

The barbell is best understood as a discipline of exposure. It asks what can kill the investor, what can be allowed to fail, and what can benefit from surprise. It rejects the idea that every dollar should be optimized for expected return. Some dollars exist to keep the investor alive. Other dollars exist to buy exposure to nonlinear upside. The danger is that investors imitate the language without respecting the severe demands of sizing, liquidity, and loss tolerance.

Antifragility and the move beyond robustness

Antifragile widened Taleb's project from finance to systems. The basic distinction is simple but powerful. The fragile is harmed by disorder. The robust survives it. The antifragile benefits from it. In markets, the idea points directly to convexity: a position or system with limited downside and expanding upside can improve when volatility rises, while a fragile system can deteriorate suddenly after a long period of calm.

This was the philosophical extension of his options background. Long optionality can lose money repeatedly before paying off, but its payoff profile can be improved by movement, surprise, and dispersion. Short optionality can look stable, but its apparent income may be compensation for bearing hidden catastrophe risk. Taleb took that options grammar and applied it to companies, governments, health, personal decisions, and social systems, sometimes persuasively and sometimes expansively enough to invite criticism.

For investors, the most useful part of antifragility is the habit of asking how a portfolio responds to error. If the model is wrong, does the position lose a little or a lot? If volatility rises, does the system adapt or break? If liquidity vanishes, does the investor become a forced seller or a buyer with cash? Taleb's lasting contribution is to make those questions prior to any forecast.

Universa and the institutional expression of tail-risk protection

Universa Investments became the most visible institutional expression of the Talebian tail-risk idea. The firm is led by Mark Spitznagel, with Taleb associated as a scientific adviser, and its public identity centers on risk mitigation rather than conventional diversification. Lionscrest, which provides access to Universa strategies for qualified investors, describes the aim as protecting capital and raising compound returns by mitigating steep portfolio losses.

The public numbers most often associated with Universa require careful language. Institutional Investor reported that Universa generated a 4,144 percent return in the first quarter of 2020, according to a client letter, and emphasized that the firm focuses on the overall portfolio effect rather than the headline return on hedge capital. The same article reported a hypothetical portfolio with 3.33 percent in Universa's tail-risk strategy and 96.67 percent in the S&P 500 had gained 11.5 percent per year since inception in March 2008, versus 7.9 percent for the S&P 500 over the same period.

Those figures are striking, but they are not a simple instruction manual. Tail-risk strategies can produce extraordinary returns on a small sleeve during crashes while still imposing a recurring cost during ordinary markets. The relevant question is not whether a hedge pays off in a panic. It is whether the investor can size it, fund it, hold it, and rebalance it so that the total portfolio compounds better over full cycles. Universa's own public framing stresses that portfolio-level effect.

The hard part is not the crash, it is the waiting

The psychological weakness of tail protection is obvious: it spends money when nothing happens. That is easy to defend in theory and hard to defend in a boardroom. Institutional Investor's account of CalPERS and tail hedging illustrated the governance problem. A hedge can look like a persistent drag, and the decision-maker paying the cost may not be the one in the seat when the crash finally arrives. Career horizons rarely match tail-risk horizons.

Taleb's answer is that insurance is not a luxury if the asset being protected is essential. Yet even that analogy has limits. A homeowner can observe a premium and a contract. A complex institutional tail hedge depends on instruments, strikes, maturities, rebalancing, liquidity, and manager skill. The cost is visible every period. The benefit is uncertain in timing and magnitude. That asymmetry makes tail hedging a test of governance as much as finance.

This is where Taleb's method has one of its central failure modes. A barbell can become a slogan for doing imprudent things with the risky sleeve. A tail hedge can become an expensive badge of sophistication. A fear of models can turn into a refusal to measure anything. The insight that rare events matter does not absolve investors from execution. It raises the standard for execution because the strategy will be most questioned precisely when it has not yet worked.

Skin in the game and the ethics of hidden risk

Skin in the Game returned Taleb's risk theory to a moral claim: those who make decisions should bear the consequences. Penguin Random House describes the book as a challenge to beliefs about risk and reward, politics, religion, finance, and personal responsibility. The finance application is direct. If bankers, executives, consultants, or policymakers gain from upside while others absorb losses, the system encourages hidden fragility.

This principle gives Taleb's work a sharper edge than many discussions of risk management. He is not satisfied with better disclosure or more elegant models if incentives remain asymmetric. A trader paid annual bonuses for selling disaster insurance can look brilliant until the disaster arrives, at which point shareholders or taxpayers may inherit the loss. A corporate executive can boost earnings through leverage or buybacks and leave successors with reduced resilience. A forecaster can be wrong without personal cost.

The strength of the skin-in-the-game idea is its clarity. It turns complex risk debates into a question of symmetry. The weakness is that real institutions often require delegated decision-making, limited liability, and specialization. Not every risk can be borne fully by its originator. Still, Taleb's standard remains a useful diagnostic: when a person or institution recommends a risk, ask what they lose if the risk materializes.

The fourth quadrant and the limits of precision

Taleb's more technical work tries to formalize where statistical confidence breaks down. In Errors, Robustness, and the Fourth Quadrant, he distinguishes between thin-tailed and fat-tailed domains and between simple binary payoffs and complex payoffs. The most dangerous zone is the fourth quadrant, where the distribution is fat-tailed and the payoff is complex. There, small errors in assumptions can produce large errors in decisions.

This framework is a bridge between his popular writing and risk engineering. It does not say that all statistics are useless. It says the usefulness of a method depends on the domain and the payoff. Casino games, laboratory settings, and some binary decisions may allow probabilities to be used with reasonable confidence. Leveraged financial systems, geopolitical risk, pandemics, and portfolios with nonlinear exposures often do not. The problem is not mathematics itself. It is the wrong mathematics in the wrong place.

The practical implication is to change the payoff when the probability cannot be trusted. If the loss is ruinous and the probability is uncertain, reduce the exposure rather than pretend to know the number. If the upside is open and the downside is capped, uncertainty may be acceptable or desirable. This is the deep link between Taleb's fourth quadrant, barbell investing, and antifragility. Each is a different way of asking how to act when the forecast is weakest.

Pandemics, white swans, and the difference between surprise and neglect

Taleb's pandemic writing showed how his ideas extend beyond markets while still returning to market structure. On January 26, 2020, Joseph Norman, Yaneer Bar-Yam, and Taleb published a note through the New England Complex Systems Institute warning about the systemic risk of novel pathogens and arguing that reducing connectivity was robust to misestimation of viral properties. The point was not a precise forecast. It was a precautionary response to fat-tailed uncertainty.

That distinction later became central to Taleb's objection to calling COVID-19 a Black Swan. A global pandemic was not beyond historical imagination. The failure was preparation, incentives, and the slow recognition of nonlinear spread. In market terms, it resembled a known class of exposure that had been underfunded because the timing was uncertain and prevention looked costly before the fact. The lesson matched his finance argument: do not wait for precision when the downside is systemic.

The same logic applied to corporate balance sheets in 2020. Firms that optimized for efficiency, leverage, and distributions to shareholders often discovered that resilience had been treated as idle capital. Taleb's critique was severe because he sees this pattern as recurring. Calm periods reward fragility. Then a shock exposes the structure. The public argument after the fact focuses on the shock, while the more important question is why so many systems were built with so little room for error.

Criticism, temperament, and statistical pushback

Taleb's influence has always come with resistance. Some critics object to his tone, which can be combative, dismissive, and personal. Others object to the substance, arguing that statisticians and financial economists were not as naive about fat tails, robust methods, or model error as his polemics suggest. The American Statistician devoted space in 2007 to reviews and responses related to The Black Swan, a sign that his claims had reached serious statistical audiences and provoked serious disagreement.

The strongest critique is that Taleb sometimes writes as if the failure of one modeling culture indicts too much of statistical practice. Markets are not casinos, but that does not mean all quantitative inference is empty. Good statisticians understand sampling error, model uncertainty, non-normal distributions, and robustness. The question is whether institutions use those tools honestly under pressure. Taleb is most convincing when attacking institutional misuse of numbers, less convincing when readers hear him as attacking nearly all formal estimation.

There is also a communication problem of success. Black Swan became such a popular phrase that it is now often used to describe any large market decline. That overuse can flatten Taleb's own distinctions. If everything surprising is a Black Swan, the concept loses discipline. If every ordinary risk warning is recast as Talebian profundity, the work becomes a brand rather than a method. The irony is that Taleb's own popularity created a new narrative shortcut to police.

What remains useful, and what remains dangerous

What remains useful in Taleb's work is the relentless focus on exposure. Before asking what will happen, ask what happens to you if you are wrong. Before admiring a return stream, ask whether it is selling catastrophe risk. Before trusting a model, ask whether the domain is thin-tailed or fat-tailed, whether the payoff is simple or complex, and whether the user has incentives to ignore the difference. These questions are not fashionable. They are permanent.

What remains dangerous is the temptation to turn skepticism into posture. It is easy to mock forecasters, harder to build resilient portfolios. It is easy to say that rare events matter, harder to pay for protection through years of apparent waste. It is easy to celebrate optionality, harder to acquire it at sensible prices. Taleb's work can be misused by investors who want intellectual cover for extreme bets, permanent pessimism, or a refusal to distinguish between uncertainty and ignorance.

The best reading of Taleb is not as a prophet of doom. It is as a theorist of survival under incomplete knowledge. His career links the trading pit, the options book, the essay, the academic paper, and the institutional hedge. The message is severe but not hopeless: do not build systems that require the future to be well behaved. Own your risks. Keep room to maneuver. Seek upside from disorder where losses are bounded. Above all, never confuse a quiet market with a safe one.

Disclosure

Educational financial journalism and market research only. Not financial, investment, trading, tax, or legal advice.